What is a network token?

A network token is similar to an acquirer token in that it reduces PCI DSS scope and improves security by swapping sensitive card data (PAN) for non-sensitive data. However, network tokens are generated by the card brands such as Visa and Mastercard. Each brand maintains its own secure repository of network tokens that serve as payment credentials. So, if a customer loses their card or it’s stolen, the brand updates their token automatically without any disruption in service.

With network tokens, merchants can:

- Reduce declined charges due to outdated credentials

- Avoid additional fees incurred using traditional tokens or PANs

- Minimize involuntary drop-offs due to outdated customer card data

- Employ multi-processor redundancy since network tokens are fully portable

Global Payments works with the card brands to provide a Card Storage Service to merchants who want to initiate transactions using network tokens. This also includes generating cryptograms, which are required for transactions that are customer initiated.

Use cases

In this section, we present some “real world” examples that can be enabled through our Network Tokens - Card Storage Service. Keep in mind that this section doesn’t cover all of the use cases.

Use case #1: Easy migration to our payment gateway

A merchant who was previously with another payment gateway provider wants to migrate all repeat payments, such as subscriptions, to Global Payments. The merchant can just provide the Funding Primary Account Numbers (FPANs). Global Payments will then convert the FPANs to network tokens on the merchant's behalf. Using network tokens results in higher acceptance rates and reduced involuntary drop-offs from continued repeat payments.

Use case #2: Automatic card management

A merchant using an account updater to keep their customers’ cards up to date wants to reduce this burden as well as improve customer service. Since network tokens are managed by the card brands (like Visa or Mastercard), token updating is done automatically by them on behalf of the merchant. This results in higher acceptance rates because it reduces declined charges due to outdated credentials. Also, if a customer loses their card or it gets stolen, the card network updates the token directly so it continues to work without any service interruption, improving customer satisfaction.

Use case #3: Multi-provider merchant

A merchant wants to use multiple gateways for fallback or redundancy purposes. This way, if one of the gateways is slow or has an outage, another provider can be used so that there’s no interruption of payment processing. Since network tokens are fully portable (unlike acquirer tokens), the merchant can use them to switch between multiple providers as needed. This can also result in greater protection of customer PCI data.

Use case #4: Fewer fees (US/Canada only)

A merchant wants to reduce the fees they have to pay for payment processing. To help with this, the merchant decides to use network tokens because they are cheaper to operate at volume with lower interchange fees compared to standard FPANs or tokens.

How does it work?

This section provides a high-level understanding of how the network tokenization process works for both customer-initiated transactions (CITs) and merchant-initiated transactions (MITs).

CITs

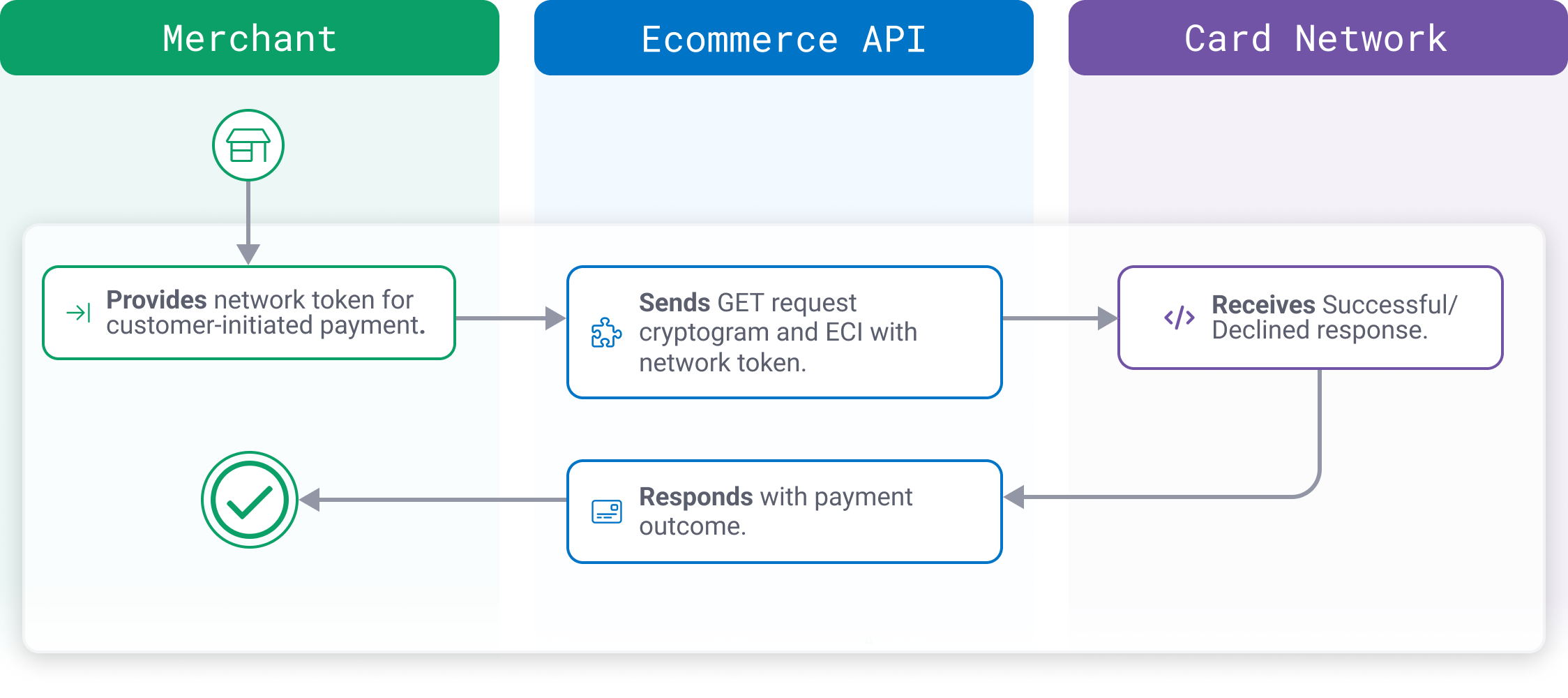

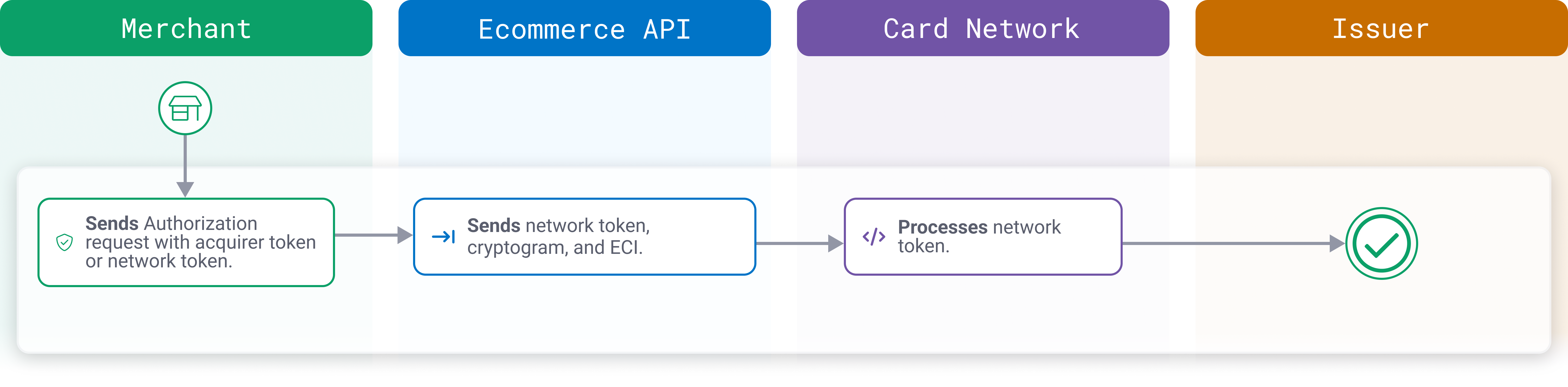

The following diagrams show the typical flow for requesting a cryptogram with an existing network token for a CIT.

Generate a cryptogram with existing network token

Make a payment with a network token

MITs

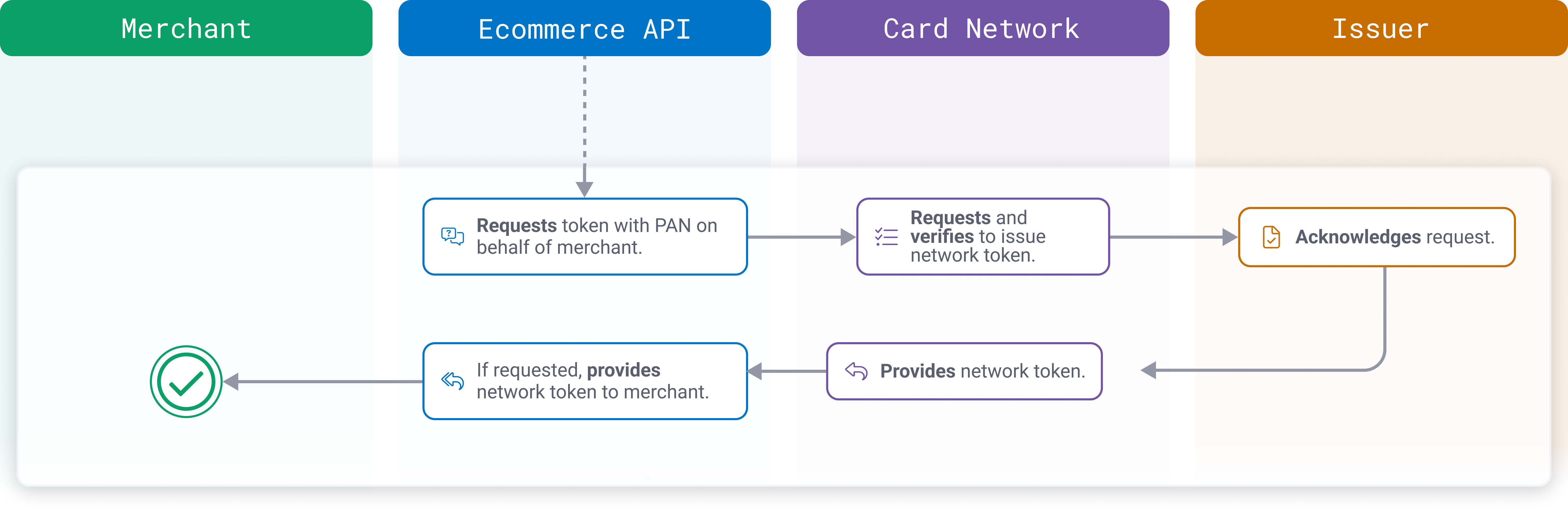

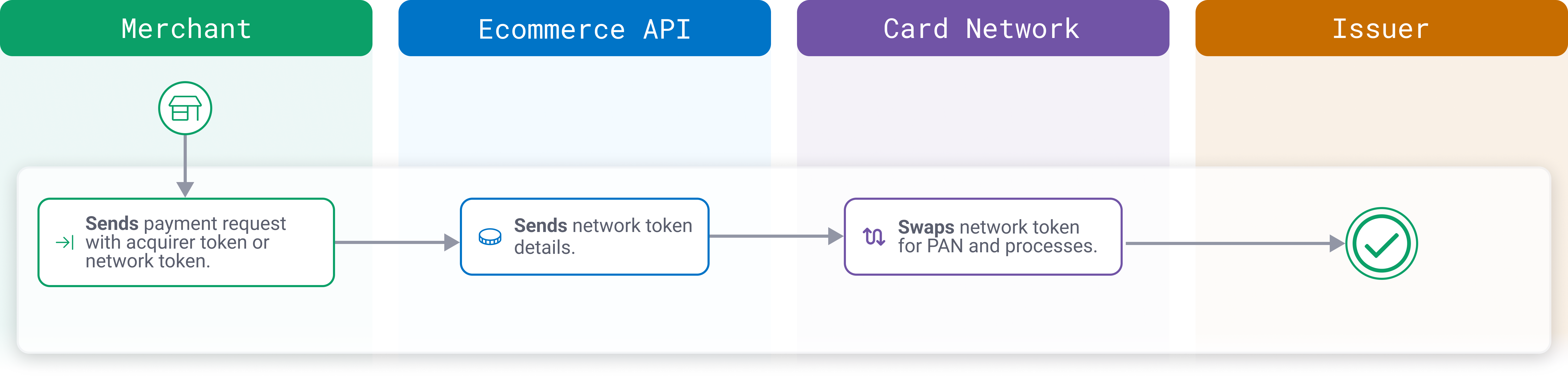

The following diagrams show the typical flow for generating a network token for an MIT.

Create a network token

Make a payment with a network token

Ready to get started?

To get started with network tokens, see our Step By Step Guide.

Remember to first register for a developer account if you don't already have one. Once logged in, you can request Sandbox credentials from the My Account dashboard.